By Topics

Overall:

0. About (10)

1. My Progress (139)

2. Car & Home (107)

3. Credit (138)

4. Banking (33)

5. Saving (49)

6. Investing (308)

7. Taxes (89)

8. Spending (74)

9. Misc (97)

A. Archive (49)

MONTHLY ARCHIVE

Feb 2014 (3)

Jan 2014 (6)

Jan 2012 (1)

Apr 2011 (1)

Mar 2011 (1)

Feb 2011 (1)

Jan 2011 (1)

Dec 2010 (1)

Oct 2010 (1)

Sep 2010 (1)

Aug 2010 (1)

Jul 2010 (1)

Jun 2010 (1)

May 2010 (1)

Apr 2010 (1)

Mar 2010 (6)

Feb 2010 (2)

Jan 2010 (7)

Dec 2009 (3)

Feb 2009 (4)

Jan 2009 (8)

Dec 2008 (1)

Jun 2008 (2)

May 2008 (2)

Apr 2008 (5)

Feb 2008 (3)

Jan 2008 (15)

Dec 2007 (32)

Nov 2007 (6)

Oct 2007 (8)

Sep 2007 (9)

Aug 2007 (24)

Jul 2007 (2)

Jun 2007 (1)

May 2007 (3)

Apr 2007 (4)

Mar 2007 (4)

Feb 2007 (13)

Jan 2007 (6)

Dec 2006 (3)

Nov 2006 (7)

Oct 2006 (7)

Sep 2006 (6)

Aug 2006 (4)

Jul 2006 (10)

Jun 2006 (1)

May 2006 (3)

Apr 2006 (2)

Mar 2006 (6)

Feb 2006 (6)

Jan 2006 (3)

Dec 2005 (1)

Nov 2005 (9)

Oct 2005 (8)

Sep 2005 (13)

Aug 2005 (25)

Jul 2005 (16)

Jun 2005 (17)

May 2005 (19)

Apr 2005 (20)

Mar 2005 (24)

Feb 2005 (23)

Jan 2005 (36)

Dec 2004 (40)

Nov 2004 (34)

Oct 2004 (17)

Sep 2004 (21)

Aug 2004 (59)

Jul 2004 (37)

Jun 2004 (31)

May 2004 (29)

Apr 2004 (52)

Mar 2004 (49)

Feb 2004 (49)

Jan 2004 (31)

Dec 2003 (48)

Nov 2003 (52)

Oct 2003 (29)

Sep 2003 (8)

Aug 2003 (5)

Jul 2003 (2)

Jun 2003 (2)

May 2003 (5)

Apr 2003 (2)

Mar 2003 (2)

Feb 2003 (3)

Jan 2003 (29)

|

|

|

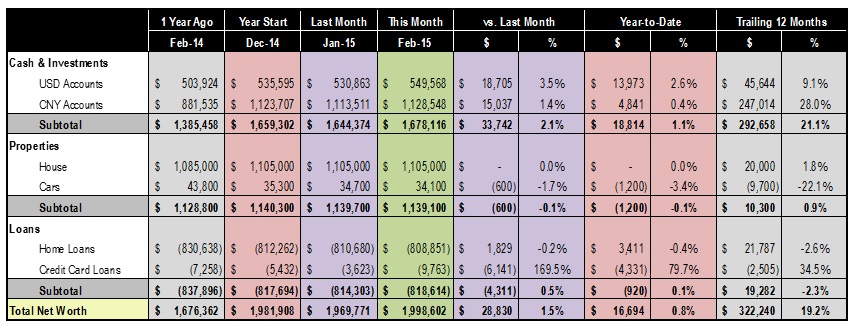

March 8, 2015 06:37 AM

Recovering from the temporary setback in January, our net worth advanced almost $29K in the month and is now tantalizingly close to $2M.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

|

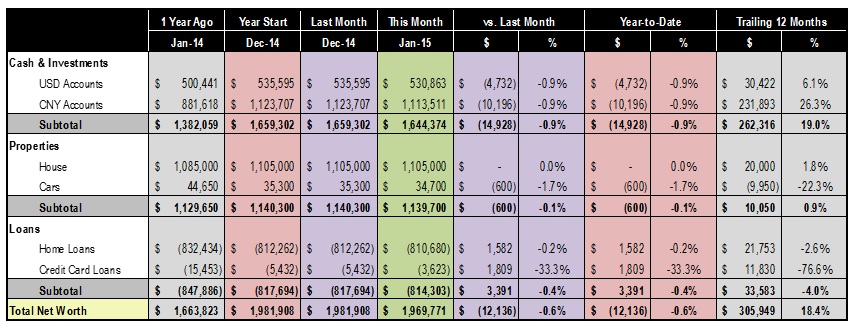

February 21, 2015 05:07 AM

Our back-to-back five-figure monthly asset growth finally came to an end. In the month of January 2015, our net worth dropped over $12K, or about 0.6%. On a trailing 12 months basis, our war chest still delivered a comfortable improvement of $305K, or 18.4%.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

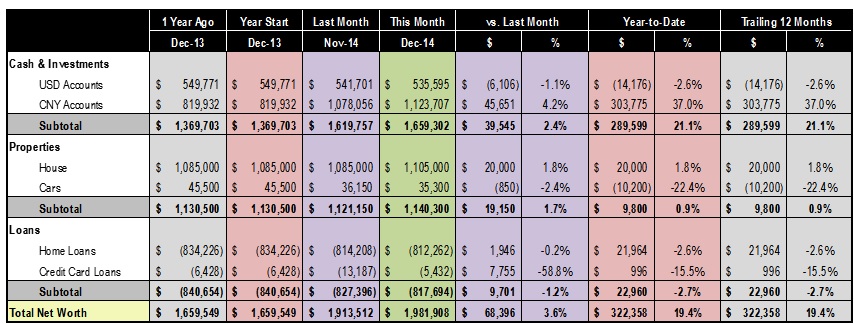

January 25, 2015 04:12 AM

Our net worth closed the year of 2014 in a high note, climbing a whopping $68K in December. For the full year, we added over $322K to our bottom line, the largest of any year in our history. In fact, we recorded 5-figure monthly improvement in 10 of the 12 months in 2014, including nine back-to-back months between Q2 and Q4 of 2014.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

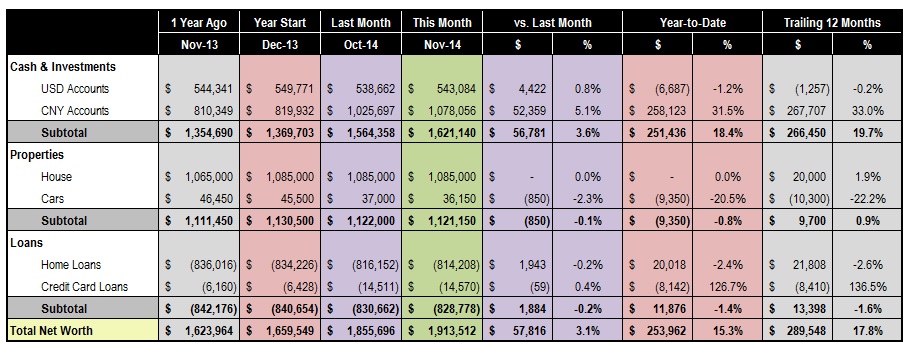

December 13, 2014 10:36 PM

November has been a great month for us. Riding on some substantial portfolio gains, our net worth climbed to a new high of over $1.9M, making this the 8th month of back-to-back five-figure growth. This year so far, we grew our financial fortune by over $250K. If 2014 ends today, it will be our largest annual gain, ever.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

November 11, 2014 05:15 AM

Our net worth continued its steady growth in the month of October. The monthly gain of $18,800 propelled our year-to-date asset growth to almost $200K, handily beating our net worth improvement of $172K in the first 10 months of 2013.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

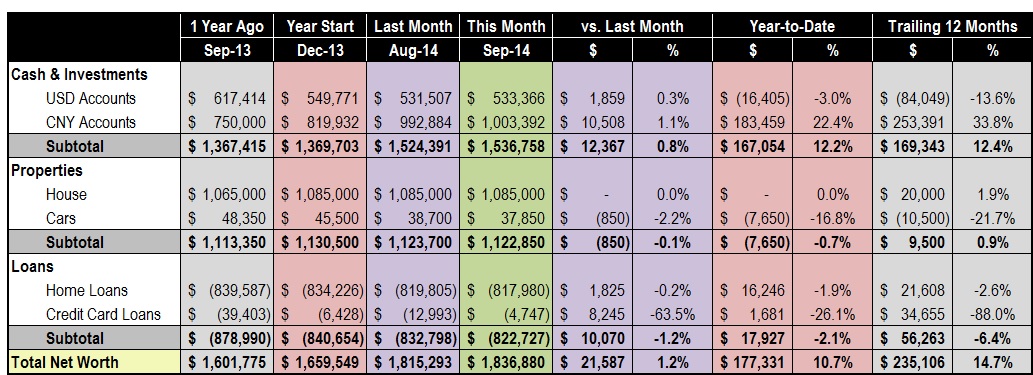

October 8, 2014 07:20 PM

Our family net worth grew a handsome $21,000, or 1.2%, in September, extending our winning streak of back-to-back five-figure monthly gains to the 6th month. For the first nine months of the year, we have grown our total assets by over $177K, besting the $146K gain in the same period last year.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

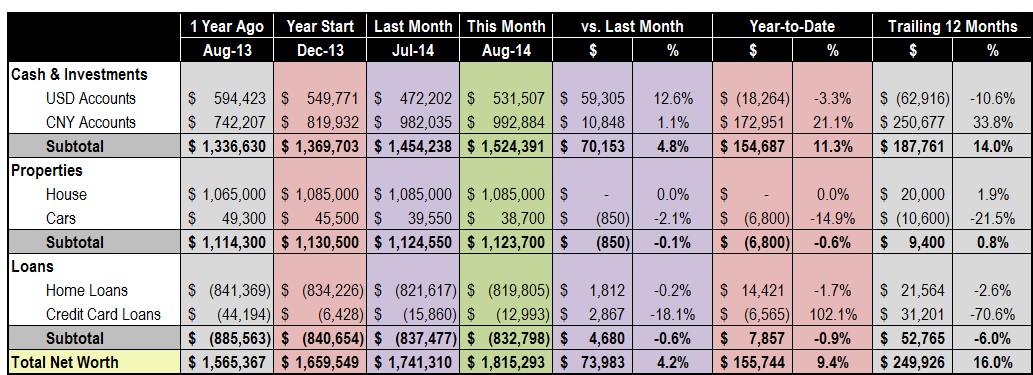

September 7, 2014 11:26 AM

Our net worth typically receives a big increase every August due to the annual vesting of stock awards from my employment. Last August, our net worth rallied $40K. The year before, it was $64k. And we are thrilled to see another $74K boost to our bottom line in the passing month.

This adds to our winning streak -- five back-to-back monthly net worth improvement of over $10K. At $1,815, our net worth gained just shy of $250K in the last 12 months.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

August 18, 2014 03:02 PM

With another $19K increase, July is the four consecutive month we enjoyed five-digit monthly net worth improvement. At $1,741K, our net worth rose a handsome $216K in the last 12 months, a good 14.2% gain.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

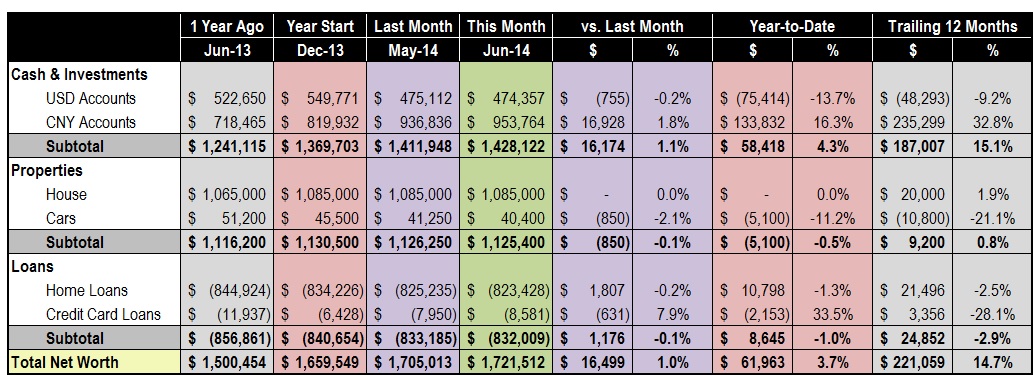

August 18, 2014 02:33 PM

We closed the month of June with a net worth increase of $16,499, or slightly below 1%. In the trailing 12 months, our net worth growth exceeded $220K, of 14.7%.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

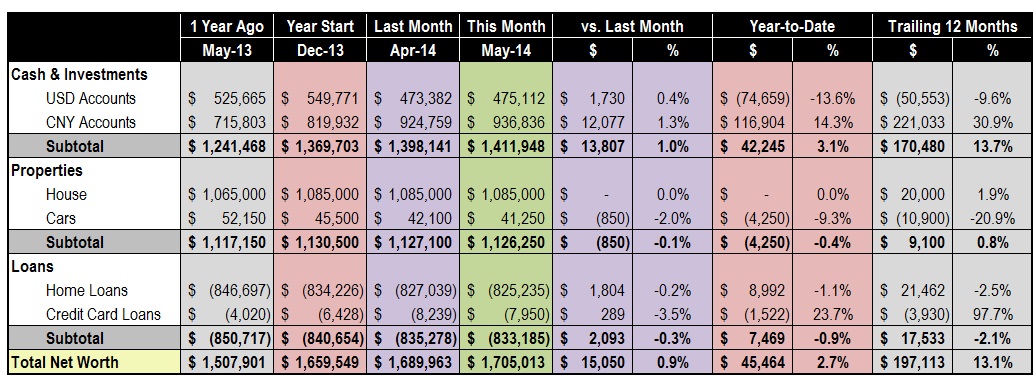

June 8, 2014 05:34 PM

With another five-figure increase in the month of May, our net worth breached $1.7M for the first time. In the trailing 12 months, we grew our net worth by $197K, or 13.1%.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

May 10, 2014 01:34 PM

After a mild setback in March, our net worth resumed its steady growth. In April with a monthly improvement of $19,015, or 1.1%, making it the best showing in the last six months.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

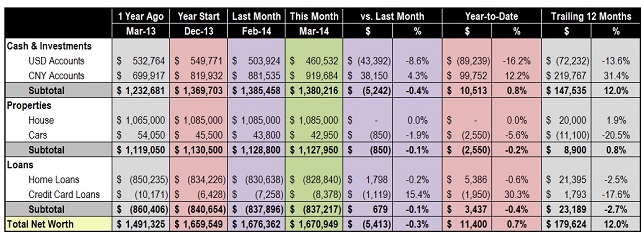

April 10, 2014 02:21 AM

Our net worth ended the month of March 2014 at $1,670,949, a slight 0.3% retreat from the prior month. All in all, we ended the first quarter of the year with a combined net worth gain of $11,400, or 0.7%.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

March 16, 2014 07:41 AM

It has been a year since we bought our new home on an acre-shy lot. I am not a particular fan of gardening over my life so far, and hence for most of last year, I had conveniently outsourced the yard work to my gardener for $330 a month, including tax. He is a good young man who bought an established lawn care business and does adequate work. I even introduced him to our neighbor across the street, from whom he won the lawn maintenance business too. By November we mutually agreed to pause the service until grass will grow again in March. I also sent him a Christmas gift card for appreciation.

March has come with a heartburning message from my gardener. Two weeks ago, I received a new proposed contract requesting a price hike of almost 50%, to $490 a month for year-long service.

I know I had a good deal in only paying $330 a month for my big yard -- I did some comparison shopping earlier in 2013 and I was quoted anywhere between $450 to $600 for comparable services. This young gentleman was just resetting his service to the market price so it is nothing wrong with him.

But still, a 50% price hike is a lot to stomach.

|

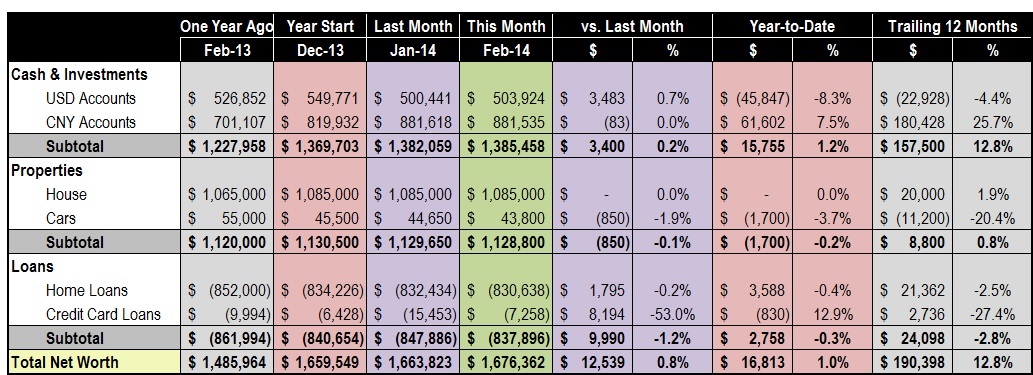

March 2, 2014 09:29 AM

Advancing $12,539, or 0.75%, our net worth closed the month of February at $1,676,362. Trailing 12 months improvement is $190,398, or 12.8%.

Our household balance sheet, along with monthly, year-to-date, and trailing 12 months comparison, are shown below:

|

February 26, 2014 06:58 AM

I spent several hours this Sunday morning to put some finishing touches to our federal tax return, and the 27-page return is now on its way to IRS this week. I have worked on the tax return since the late January, and by my estimate, I spent around 20 hours on TaxAct to prepare the return, not to count the time throughout the year with Quicken to keep a clean financial record. This is higher than the 15 hours average time burden for filing a tax return on 1040 as estimated by IRS. Maybe I could work on my math in the coming year so I can beat the average :-)

I enjoyed acquiring tax knowledge and preparing my own tax, and I put it to good use in filing the 2013 tax return. 2013 is a year of change for us thanks to the relocation, home buying and car purchase, and throughout the year, whenever I come across a personal finance article on tax that reveals something that might apply to our case, I usually do additional research and put a note to my OneNote so I can remind myself when I start to work on the actual return.

|

February 17, 2014 08:07 AM

As part of the HELOC application process, we were asked to sign a 4506-T form to authorize banks to get from IRS transcripts of our prior years' tax returns. This makes me think: as taxpayers, can we get such information ourselves?

Yes, we can.

A quick search on the IRS website yields two different options:

1) One may request a tax return "transcript" for free. A "tax return transcript" contains "most line items from your tax return (Form 1040, 1040A or 1040EZ) as it was originally filed, including any accompanying forms and schedules."

2) Or, one may order an exact copy of tax return, which includes all attachments like W-2. There is a fee of $50.00 for each tax year requested, though.

|

February 14, 2014 03:52 AM

As each of us are making progress in our respective tax returns, this MarketWatch article conveniently reminded us that it has been 100 years since Americans started paying federal income tax.

Many intriguing facts from the article and the slide show covering the evolution of Form 1040 over the past century. Some fascinating facts I learned by reading this article and doing some additional research:

1) The first-ever Form 1040 (of tax year 1913) was only three page long with one page instruction and no additional forms or schedules. Today: it's two pages but with 206-page instructions, not counting additional forms and schedules and their accompanying instructions.

|

February 13, 2014 04:33 AM

When we purchased the our house back in January 2013, we put 20% down payment to secure an ultra-low 1.875% APR 7/1 ARM. In anticipation of potential carry trade opportunities, I'm also exploring possibilities to cash out some of our home equity through HELOC, or Home Equity Line of Credit.

HELOC offers homeowners the flexibility to borrow against their home equity at a variable rate often pegged to a major lending rate index. It works much like a credit card, so over a pre-defined "borrowing period," the borrower can borrow and repay up to a credit limit multiple times. (Its sibling, Home Equity Loan, works more like a mortgage where one borrows a lump-sum upfront at a fixed rate.)

Back in 2004, I established an HELOC account at my local credit union with a credit limit of $30,000. Although I never got a chance to tap into the credit, I see it as a good insurance against occasional liquidity crunch.

|

February 12, 2014 05:45 AM

One book I'm reading lately is Early Retirement Extreme by Jacob Lund Fisker. The book asserts that one can have an "extreme" early retirement by accumulating wealth thru only 5 years of work, and choosing to lead a meaningful retirement life while spending low to the tune of $20-30K a year.

If you think it is another personal finance book about how to save, invest and retire, you are wrong. The book is written in a more academic fashion than I thought, full of philosophical discussion and historic references. Even though I'm only 80 pages into this 238-page book, I found enough "nuggets" that are thought-provoking and challenge me to revisit my more "traditional" path toward early retirement. For a quick recap, take a look at this wiki page about Early Retirement Extreme, or ERE.

|

February 11, 2014 04:00 AM

I have been pondering the idea of USD/Chinese Yuan carry trade for a while now. The investment thesis is one can borrow USD on the cheap and put to investment vehicles denominated in Chinese Yuan with much higher return. And assuming the Chinese Yuan will keep its secular trend to become stronger vs. USD over time, or at least stay flat, one can pocket a decent return from such arbitrage.

Having been exposed to the Chinese financial market for over a decade, I see quite a lot of attractive investment options yielding 8% or higher with minimal risk lately. The other piece of the carry trade puzzle, is how to borrow US dollars at the lowest cost possible.

One source I'm looking at is Interactive Brokers. Interactive Brokers probably is not as well-known as TD Ameritrade, E*Trade, Fidelity or Charles Schwab, but it offers a wide menu of investment options at commission rate as low as $1 for 100 shares of stock (it does charge a monthly minimal commission of $10 if account value is under $100,000 though).

|

More Entries

(02/10) Adjustable Rate Mortgage: What's the Worst Case Scenario

(326 comments)

(02/09) Financial Education for Teenagers

(315 comments)

(02/08) How Many Networked Devices Do You Have In Your Household?

(58 comments)

(02/07) P2P Lending in China

(1195 comments)

(02/06) Washington State GET Is a Loser's Game, Part II

(371 comments)

(02/05) Washington State GET Is a Loser's Game, Part I

(1045 comments)

(02/04) The Cell Phone Plan for Cheapskates

(58 comments)

(02/03) Will You Accept An Amazon Prime Price Hike?

(51 comments)

(02/02) Monthly Update - January 2014 ($1,663,823, +$4,273)

(2432 comments)

(02/01) Is It Worthwhile To Keep All Receipts In Order To Maximize Sales Tax Deduction?

(250 comments)

(01/31) MyRA: What's In It For Us?

(196 comments)

(01/30) Getting Mortgage On the Cheap

(359 comments)

(01/29) Finding the Most Suitable Mortgage

(207 comments)

(01/28) Buying A House with Flat Fee Realtor

(360 comments)

(01/27) 2013 Year-End Update ($1,659,549)

(183 comments)

(01/26) Act II: Back to the (Blogging) Business …

(1430 comments)

(01/02) 2011 Year-End Update ($1,212,450)

(1383 comments)

(04/09) Monthly Update - March 2011 ($1,149,008, +$2,362)

(412 comments)

(03/05) Monthly Update - February 2010 ($1,146,646, +$19,373)

(1669 comments)

(02/05) Monthly Update - January 2010 ($1,127,273, +$4,906)

(353 comments)

(01/01) Monthly Update - December 2010 ($1,122,367, +$37,499)

(593 comments)

(12/03) Monthly Update - October/November 2010 ($1,084,868)

(474 comments)

(10/05) Monthly Update - September 2010 ($1,067,889, +$47,223)

(689 comments)

(09/17) Monthly Update - August 2010 ($1,020,665, +$34,678)

(386 comments)

(08/02) Monthly Update - July 2010 ($985,987, +$24,773)

(441 comments)

(07/09) Monthly Update - June 2010 ($961,214, -$4,421)

(513 comments)

(06/07) Monthly Update - May 2010 ($965,329, -$45,686)

(382 comments)

(05/09) Monthly Update - April 2010 ($1,011,016, +$6,626)

(442 comments)

(04/07) Finally, A Million!

(1149 comments)

(03/12) 1-Year and 10-Year Mutual Fund Performance Figures Skewed

(2345 comments)

(03/10) BofA Put an End to Overdraft Fee

(126 comments)

(03/08) Shiller vs. Siegel

(263 comments)

(03/07) Warren Buffett's 2009 Annual Letters to Berkshire Shareholders

(509 comments)

(03/03) Monthly Update - February 2010 ($984,687, +$14,331)

(510 comments)

(03/02) A Price Hike from Citi and One Less Customer

(175 comments)

(02/05) Monthly Update - January 2010 ($970,356, +$452)

(1792 comments)

(02/05) Fidelity Offers $7.95 Commission and Free ETF Trades

(198 comments)

(01/25) Losing 37% a Year for 10 Years Straight

(372 comments)

(01/21) Berkshire Hathaway Completed 50-for-1 Split

(437 comments)

(01/11) Income Tax Law Changes in 2010

(190 comments)

(01/11) Maximizing Stock Option Value: The Tax Consequences

(370 comments)

(01/08) Morningstar Announced Fund Managers of the Year 2009

(357 comments)

(01/06) Writing Option to Improve Option Value

(451 comments)

(01/06) Maximizing the Value of Expiring Employee Stock Options

(409 comments)

(12/30) Net Worth Trend: '07-'09

(330 comments)

(12/30) Decade's Winners and Losers

(98 comments)

(12/28) Decade of Progress

(1164 comments)

(02/04) How Much Are Credit Card Issuers Charging Merchants?

(416 comments)

(02/03) 100 Best Companies to Work For (2009 Edition)

(258 comments)

(02/02) What You Should Know About 2008 Individual Income Tax Returns

(2274 comments)

This page was last rebuilt at July 14, 2020 12:00 AM PST.

|

|

RSS FEED

PERSONAL FINANCE BLOGS I READ

Consumerism Commentary

Get Rich Slowly

My Money Blog

All Financial Matters

The Simple Dollar

|